Show me the money

a Gen-Z take on what I did with my rands that just made sense

Rands & Sense is an independent financial literacy initiative. It is not affiliated with, endorsed by, or connected to any financial institution. The content provided is for educational purposes only and does not constitute financial advice. All concepts discussed are based on publicly available information and widely accessible market resources. Sources and references are available where relevant.

Don't leave money on the table

A reminder: I am NOT a financial advisor, and nothing on this site is financial advice.

I share financial literacy content for educational purposes only, and I also want to be clear that I do not want to create the perception that I am acting as a financial advisor or am affiliated with any institution.

But managing my money was a HUGE priority as soon as I had some in the bank. And it should probably be a priority for you too!

Do you want to be part of the 51% of South Africans that are empowered to make financially sound decisions?? Trick question, of course you do.

My life story is not yours. The way I manage my finances may not be appropriate for everyone. But based on principles I’ve learned from publicly available research, widely discussed financial education resources, and commonly referenced personal finance literature, I’ve condensed some of the concepts that shaped how I think about money into the steps below.

Think of this less as advice and more as a financial literacy crash course built from things I’ve learned along the way.

Read on for more insights…or just an entertaining piece jampacked with all things Gen-zennial.

All of this content is based on these resources

None of my ideas are original (I’m not smart enough for that). But hopefully I can put them forward to you in an original format. You should check them out for yourself!

Starting with the basics

Interest and Inflation

Inflation is basically how fast prices go up over time. In South Africa, it’s measured every month by Statistics South Africa using the Consumer Price Index (CPI).

So if inflation (CPI) is 6%, that Labubu that cost R100 a year ago now costs roughly R106.

Buuut… if your savings grow slower than inflation, your purchasing power goes backwards. That’s just a fancy way of saying if your money didn’t also grow by 6%, guess what?

No Labubu for future you.

That said, inflation isn’t the villain people make it out to be. In fact, zero inflation can actually be a problem for an economy (see Japan). When people expect prices to fall or stay flat forever, they stop spending, businesses stop investing, and growth stalls.

What you want instead is a Goldilocks situation. Enough spending to keep the economy moving, but not so much that prices run wild. And mama-bear SARB manages this by setting targets inflation targets and messing with the interest rate.

For context, as of December 2025 the average inflation rate dipped to a 21-year low of 3.2% and the CPI for Ke Dezemba was 3.6%. Enoch Godongwana announced a new inflation target for South Africa of 3% with a 1 percentage point tolerance band back in November 2025.

Side Note: how did we come up with a target?

The TLDR version is that 30 years ago, a bunch of people in New Zealand were grappling with double digit rampant inflation. So monetary policy makers thumbsucked a figure of 2% to aim towards.

Why 2% you ask? Good luck finding an answer to that! And yet somehow for the past 30 years, that 2% has been a target adopted by economies all around the world.

Why should you care?

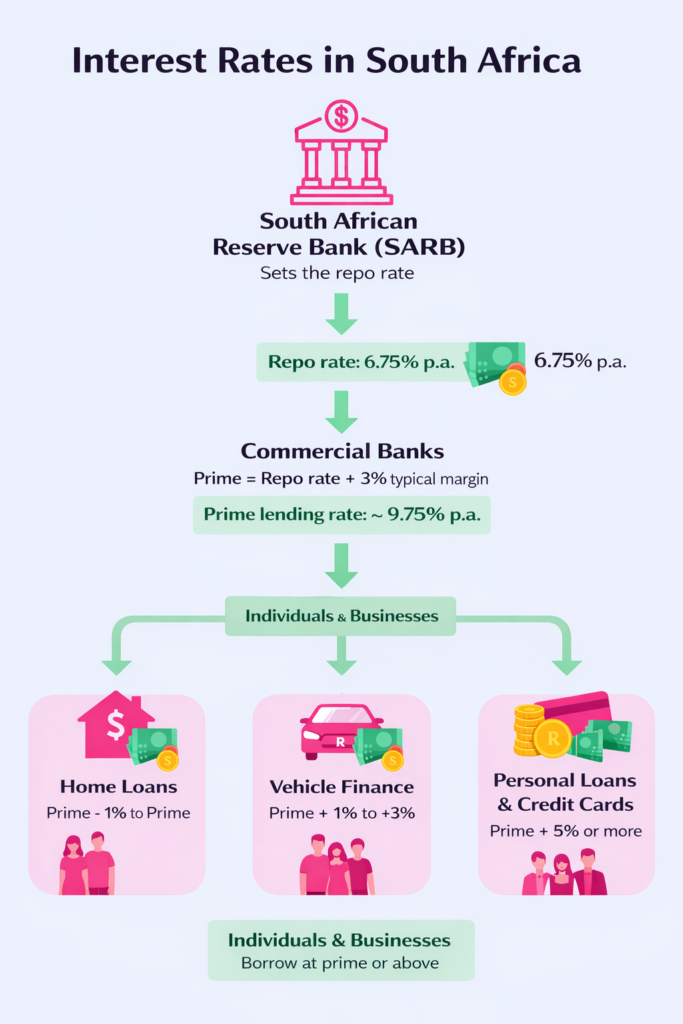

The South African Reserve Bank (SARB) is South Africa’s central bank. The big kahoona. It’ s job is to manage monetary policy, control inflation and oversee financial stability.

So how does SARB actually control inflation?

They set the repo rate which is the rate at which commercial banks borrow short-term money from SARB. When the repo rate is, say, 6.75%, banks can’t exactly lend that money out at the same rate and call it a day. The big man still has overheads.

That’s why banks lend to customers at the prime rate, which is usually repo + a margin. Right now, that puts prime at around 10.25%.

Now here’s where you come in.

When you park your money in a savings account at Bank XYZ, the interest you earn is usually well below prime and often closer to the repo rate (or even less).

Banks make money on the spread:

what they charge borrowers (prime + margin)

versus what they pay depositors (your savings rate)

The big man gotta eat too!

That said, a savings account is still a relatively safe place to store your money. The risk of one of South Africa’s Big Four banks failing is low, thanks to strong regulation and global banking standards like the Basel III Accords. Low risk doesn’t mean NO risk though, SA’s deposit insurance scheme is capped at a 100k payout if your bank can’t give you your money back.

But the real question is this:

Will the interest you earn beat inflation by enough to make you a baller?

And could your money be working harder elsewhere?

Read on for Risk vs Reward.

Pay yourself first

Before we talk about reward lets talk about risk. Particularly the risk you face by just being alive and living your life.

You need an emergency fund.

Building up an emergency fund of 3–6 months’ worth of living expenses was the very first thing I did before even thinking about all the fancy investing stuff.

And for good reason.

In South Africa, around three-quarters of adults who take on credit use it to cover basic necessities like food, transport, and utilities. On top of that, over 10–12 million adults are considered over-indebted. The absolute last place you want to be is going into debt just to survive, especially if you come from a relatively well-off position.

Yet here’s the wild part: nearly 1 in 3 high-income South Africans have no emergency savings at all. Even more concerning, banking industry surveys show that more than half of entry-level private-banking clients have less than one month’s salary in accessible cash.

A big lesson from The Richest Man in Babylon (and from my dad): Pay yourself first.

It doesn’t have to be dramatic. Even a small, consistent amount put aside for you can save you when life inevitably happens, like when your car has a little oopsie after meeting a curb.

Many people choose to keep an emergency fund in an easily accessible savings account so that unexpected expenses can be covered without additional stress or debt.

One very important reminder:

Your savings are NOT your emergency fund.

Your emergency fund is your safety net — 3–6 months of living expenses for when things go south.

Your savings are the cash you put aside monthly (often around 15%, according to people like Ingram and plenty of others) for goals… or that minted R15k Labubu.

Put the credit card down!

As Warren Ingram puts it: Debt is the biggest destroyer of wealth. People don’t just stress about debt, it literally ruins lives. He suggests that you should avoid Bad Debt as much as you can.

Bad Debt is basically high interest short term debt– think credit cards, personal loans, store cards and microloans. Yoh guys these things are dangerous. Interest rates here tend to attract the highest interest payable between 15%-20%.

If you have to take out a loan to go to Cape Town for ke Dezemba, you can’t afford it. Respectfully (RIP).

Some people choose to use a credit card as a way to build a credit profile and to benefit from the additional security that credit cards can offer for online purchases (hello fraud protection).

A commonly discussed approach in personal finance education is to ensure that the full balance is paid off each month, which can help avoid interest charges and support responsible credit use. Very cutesy. Very demure. Very disciplined.

Medium term debt are for things like cars finance and Ingram suggests only spending 20% of your salary on repayments.

We can survive without you revving your M2 at The Pantry and Relish if you’re not suffocating every month. Ideally you’d also put down a large deposit which reduces:

- your monthly repayment

- total interest paid

- the risk of owing more than the car is worth

Long term debt could be considered good if its used to buy a value appreciating asset, like a home. And even then, it’s not automatic wealth. Ingram does a pretty convincing analysis of why property might not be the best investment for a young professional. And buying a home will likely be the biggest financial decision you make in your life, so it’s important to consider your options wisely.

Yes, property can grow in value over time, but only if you can comfortably afford:

- bond repayments

- rates & taxes

- maintenance

- insurance

- and still save

Student loans

Unfortunately it’s unrealistic in a country like South Africa to just say “don’t have debt” and call it a day.

The majority of students are up to their necks in student loan debt with over 600k students applying to NSFAS.

One of my favorite youtubers Dave Ramsey Has extremely practical advice on how to reduce debt and the methods you can use to keep yourself afloat. Some might make the argument that student loans can be seen as an investment IF you choose to study a profession with high earning potential.

For example, the South African Institute of Chartered Accountants runs a bursary scheme called Thuthuka which specifically funds and assists students in paying for their tuition to study chartered accounting. Thuthuka has played a role in changing the course of so many lives so you should consider donating today.

now that the foundations are covered

Investing (finally!)

Folks, I know that I am not an asset fund manager. I do not have the time in my day to be refreshing BusinessLive and the Financial Times to try and predict which way the market is going to swing. In fact, it is such a time-consuming task that people have entire careers dedicated to doing exactly that.

I am too busy getting dirty chais and iced matchas from a coffee shop (and adding shareholder value, of course) to be that plugged in. And chances are, you are too.

It is very unlikely that an individual investor managing their own portfolio will consistently outperform professional traders who have access to institutional research, live market data and teams of analysts.

Because of this, many investors focus less on trying to predict short-term market movements and more on staying invested over longer time horizon. That inherently means taking a medium to long-term view and letting time do most of the heavy lifting.

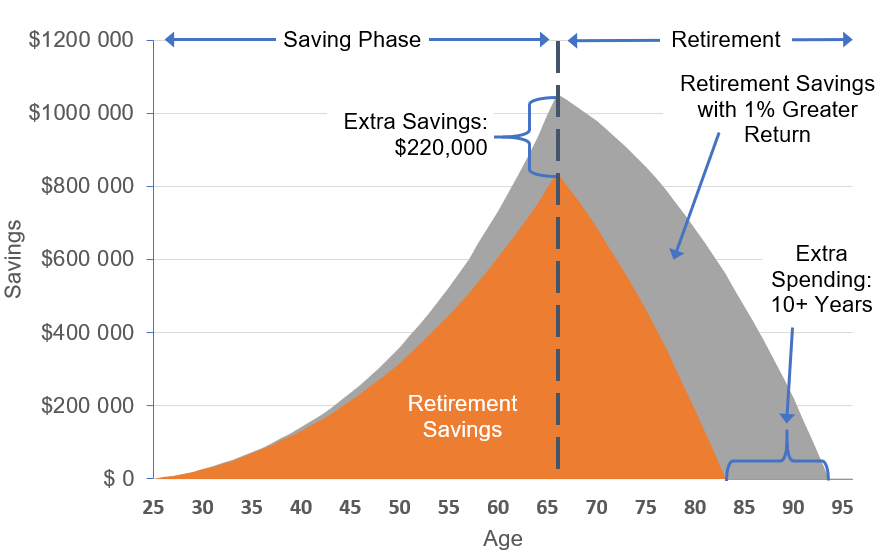

Invest early and consistently

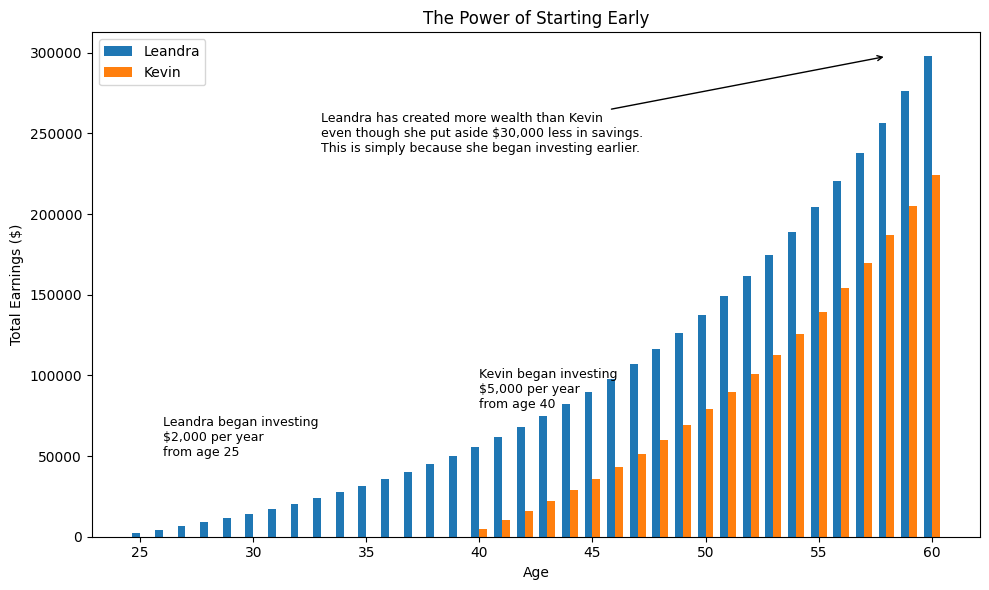

If there is one thing that matters more than picking the “perfect” investment, it is starting early and staying consistent.

The graph above illustrates this point nicely. Leandra starts investing earlier, even though she contributes less overall, and still ends up with more wealth than Kevin. This is not because she is smarter or takes more risk. It is simply because her money has more time to compound.

Important disclaimer before anyone comes for me: this is a simplified illustration. Real markets do not grow in smooth, straight lines. Returns fluctuate, inflation exists, taxes exist, and there are fees involved. The point of the chart is not to promise guaranteed outcomes, but to show the power of time in the market.

Sometimes you do not even have to think very hard about which specific company to invest in, especially if you do not have the time or desire to spend hours digging through industries, reading annual financial statements cover to cover, or refreshing SENS announcements hoping to catch the next big story.

That is where index funds come in.

One of the reasons index investing is widely discussed in financial education is that researching and selecting individual companies can require significant time, analysis, and expertise. For many investors, consistently identifying companies that outperform the market is difficult.

When you buy a share, you are buying a piece of a business. You are effectively handing your money to the managers of that company and trusting them to allocate capital in a way that creates more value over time.

Index funds take a different approach. Instead of trying to pick individual winners, they aim to track the performance of a broad market index by holding many companies at once.

How you actually make money as a shareholder

There are two main ways to earn a return on shares.

- Share price appreciation

This happens when the market value of the company increases. It is tempting to assume that good financial results automatically lead to a higher share price, but that is not always the case.

As Aswath Damodaran puts it, financial statements help anchor valuation, but prices are set by markets that reflect expectations and perceptions as much as fundamentals.

A company can report strong results and still see its share price fall if those results disappoint relative to what the market expected.

- Dividends

Dividends are cash payments made to shareholders at management’s discretion after all obligations have been met. Even if a company is profitable and has no debt issues, it is not required to pay dividends.

As a shareholder, you sit last in the capital structure. Everyone else gets paid before you. Creditors, employees, suppliers, SARS. You are at the bottom of the waterfall.

That said, companies often choose not to pay dividends because they believe reinvesting that money will generate higher long-term returns. Dividends are nice, but they are not free money. They come with trade-offs.

Price ≠ Value

One of the most important investing lessons is that price does not equal value.

Financial statements can help estimate what a company might be worth based on its fundamentals. The share price, however, is simply what buyers and sellers agree on today. That price is influenced by sentiment, narratives, fear, hype, and vibes.

Sometimes you get lucky and invest in something the market loves. Sometimes you lose money because expectations change. High risk, high reward. The game is the game.

index funds

What are index funds and how do they work?

Back in the olden days (the 70s), a man named Jack Bogle founded an investment firm called Vanguard. This man is largely credited with popularising what we now know as the index fund for everyday investors. The idea was instead of trying to outsmart the market, you just track it.

An index fund is basically a rules-based basket of shares that mirrors a specific market or segment of the market. So no stock-picking stock XYZ when the time feels right.

Some common examples:

- S&P 500: roughly the 500 largest US companies

- Nasdaq-100: 100 large non-financial companies listed on Nasdaq

- FTSE/JSE Top 40: the 40 biggest companies listed on the JSE

There is an unholy amount of evidence showing that simply parking your money in a low-cost S&P 500 index fund beats the majority of active investors over the long term (which means a decade or more).

Most active fund managers, charge relatively high fees and still fail to outperform their benchmarks once you account for those fees.

I’m not saying all active managers are bad or that none of them ever outperform. Some absolutely do. But sustained outperformance, net of fees, over long periods is rare. This is backed up year after year by the S&P Dow Jones Indices SPIVA reports, and it’s a global trend, not just a South African one.

And fees matter a lot. Fees compound in the same ugly way returns do, just in reverse. A 1 to 2 percent difference in annual fees over 30 years can leave you with dramatically less money at the end.

It's ok to be boring!

You might be skeptical. Johannesburg is filled with finance bros on TikTok who may be touting a get-rich-quick scheme encouraging unsuspecting investors to either invest in a specific stock, or invest in their course telling you how to choose a specific stock. Some may very well have beaten the market…but if you had the magic rule book to make you rich it’s very unlikely you’d be advertising it to your 1500+ followers on Instagram.

It’s also fairly easy to sell the facade of being a finance guru that retired at the tender age of 24. A reminder that it costs about R10k to rent a Porche 911 for a day, talk about living la vida loca. Even worse, many young South Africans might find themselves in debt trying to keep up with a lifestyle they simply can’t afford for appearances.

Investing might seem unsexy compared to the speculative trading, but there’s a lot of merit in playing the long game.

Warren Buffett famously made a bet in 2007 with a group of very confident hedge fund managers. Everyone started with $1 million and had ten years to see who could come out ahead. The hedge funds did what hedge funds do, lots of trading, lots of complexity, lots of fees. Buffett did absolutely nothing interesting. He just put his money into a low-cost S&P 500 index fund.

Ten years later, in 2017, Buffett won. By a lot. Net of fees. Effortlessly. Sucks to suck.

Back home, if you look at some traditional investment products, you’ll often find minimum monthly contributions or lump sums required just to get started. For many people, that can be a barrier to entry.

Because of that, a lot of newer investment platforms and funds have emerged that allow people to start with smaller amounts and lower fees, which has made investing more accessible to everyday investors.

To be clear, this isn’t about dunking on active fund managers. Active investing absolutely has its place, and many investors choose it. The important thing is understanding the different approaches and deciding what aligns with your goals.

Another widely discussed concept in investment education is passive investing, which typically involves tracking a market index rather than trying to predict which individual stocks will outperform.

Passive investing through index funds or ETFs is boring by design. You track a benchmark, turnover is low, fees are low, and you accept the market return minus minimal costs. Over long periods, that consistency plus compounding often leads to better outcomes for many investors. Not because it’s risk-free, because it’s not. Markets fall. But discipline, time, and low fees do a lot of heavy lifting.

If you’re a normal, everyday investor who just wants exposure to the biggest companies on an exchange, one commonly discussed approach in financial markets is investing through an ETF. An ETF is a fund that tracks an index like the S&P 500 and trades on the JSE like a share. You’re buying units in a fund, not individual companies directly, but that fund owns the underlying shares.

One of the key concepts often associated with index investing is diversification. For example, an index such as the S&P 500 represents exposure to hundreds of large companies. This means that the performance of a single company typically has a smaller impact on the overall portfolio compared to holding only one or two individual shares. So when something absolutely brazy happens in the world, your portfolio does not immediately go into cardiac arrest.

dollar cost averaging

Time in the market beats timing the market

Let’s say I’ve convinced you of the power of compound interest. Starting early and being consistent is the secret sauce to getting your money to actually do something.

You might still think: “Maybe I should wait until the cost of the index fund XYZ ETF is cheaper”

Again and again, it’s been proven that trying to predict when the market is “on sale” so you can perfectly time your ETF buys usually leaves people worse off in the long run. Not because they are stupid, but because markets are unpredictable and humans are emotional.

There’s also a stat people love to ignore. A tiny number of the best days in the market drive a huge chunk of long term returns. If you miss just the 10 best days over a long period, your returns drop dramatically. Those days usually happen right after market crashes, when everyone is scared and sitting on the sidelines. If you are trying to time the market and you are out at the wrong moment, you do not just miss a good day, you miss the recovery.

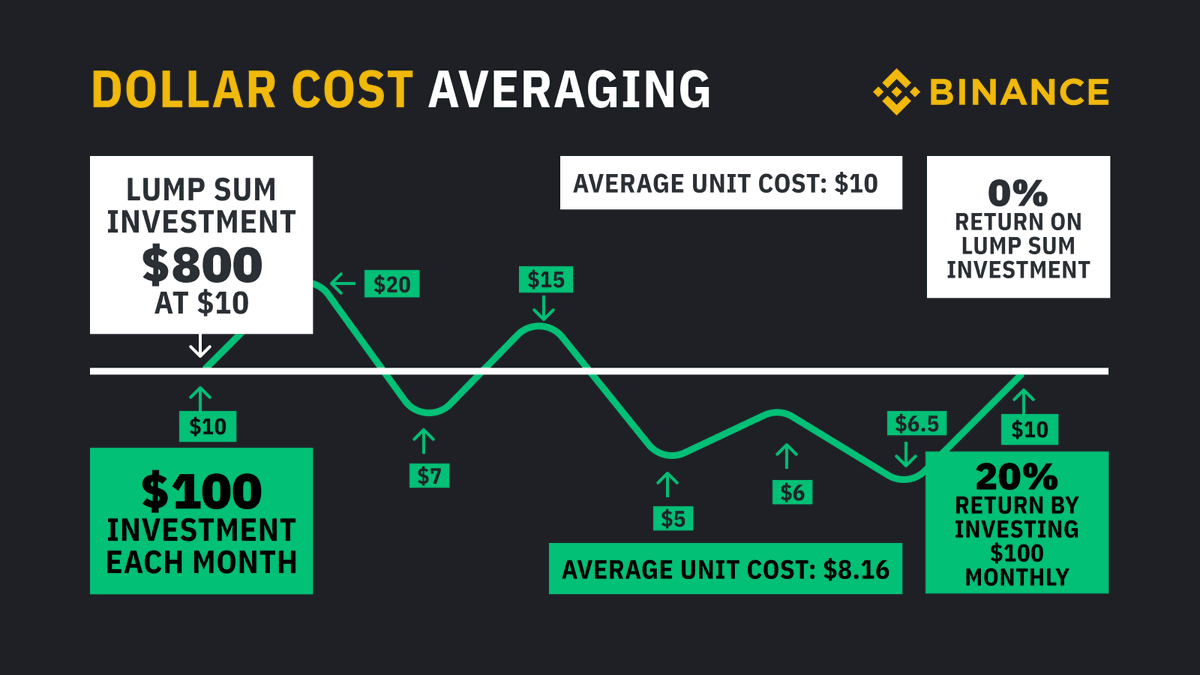

This is where dollar cost averaging (DCA) comes in. Over the long term, you might do slightly worse than investing a lump sum all at once, but that’s not really the point. DCA is a behavioural tool. By investing a fixed amount every month via debit order, you average out your cost per unit over time. That means it matters a lot less whether you bought at the “right” moment or not.

There is solid evidence showing that lump sum investing tends to outperform DCA over long periods, but it also leads to larger losses in some of the worst market environments. If you are loss averse, not glued to markets, or simply want something sustainable you can stick to, DCA often makes more sense in real life.

Tax free savings accounts

Max out your tax free savings account!

Do you like giving the government your money? If you are like most people, probably not.

A Tax Free Savings Account (TFSA) was introduced in South Africa in 2015 to encourage people to save. I don’t think most people realise just how much we are taxed. It’s literally called gross income because it’s gross to see how much you could have made.

A TFSA allows you to earn interest, dividends, and capital growth completely tax free.

As things stand:

Annual contribution limit: R46,000

Lifetime contribution limit: R500,000

If you max out your TFSA every year, you hit the lifetime limit in about 14 years. Quick maths.

How much tax would you pay without a TFSA?

The Income Tax Act is refined to a tee. Any time a loophole pops up, SARS stitches it right back up.

Here’s why a TFSA matters.

Interest tax

If you put money into a normal savings account, the interest you earn is taxable once you exceed the annual exemption:

- R23,800 if you are under 65

- R34,500 if you are 65 or older

Anything above that is taxed at your marginal income tax rate.

Dividends tax

If you invest in shares, ETFs, or index funds outside a TFSA and receive dividends:

- Dividends are taxed at 20%

- This is a withholding tax, so you often do not even see it leave

Capital gains tax (CGT)

If you buy an investment low and sell it higher, congrats, you made a capital gain. SARS would also like a congratulations fee.

For individuals:

- 40% of the gain is included in your taxable income

- That portion is then taxed at your marginal rate

- You do get a R40,000 annual CGT exclusion, but after that it adds up quickly

If you had a TFSA:

- No interest tax

- No dividends tax

- No capital gains tax

- Compounding happens without friction

Every rand stays invested. Over 20 or 30 years, that difference is massive. ETF growth inside a TFSA can fund varsity fees, a home deposit, or financial independence without SARS taking a cut.

IMPORTANT CAVEATS

- The R500,000 lifetime limit does not reset, even if you withdraw money

- If you contribute more than R36,000 in a tax year, the excess is hit with a 40% penalty

- Once you waste TFSA space, you cannot get it back

closing off

Be a lifelong learner!

This post was just an appetizer into the world of financial literacy. If you enjoyed it and laughed at least once, consider sharing it with a friend.

There’s a lot more coming. I’ll be updating this space as I learn, unlearn, and figure things out in real time.

So hang around, stay curious, and remember: if it don’t make rands, it don’t make sense!

Bring Financial Literacy to Your School or Organisation

Tailored talks and workshops for schools, universities, and early-career professionals